You open the mail and find an official-looking notice. Or maybe you’re refinancing, selling your home, or checking county records when someone tells you there’s “something filed against the property.”

Your mind probably jumps ahead.

Can they take my house? Is this even real? How long has this been there?

Take a breath.

A lien, judgment, lawsuit notice, or unfamiliar deed filing deserves attention, but it doesn’t automatically mean you’re about to lose your home. Your first job isn’t to solve the entire problem in one afternoon. It’s to identify the document, verify that it’s legitimate, and find out whether a deadline is attached to it.

Here’s how to work through that process without overlooking something important—or paying someone before you understand what you’re dealing with.

Start With the Actual Document

A letter saying something has been filed isn’t necessarily the filing itself.

Before you call the person demanding money, negotiate a settlement, or assume the worst, get a complete copy of the recorded document from an official source. Depending on the filing, that may be your:

- County recorder or recorder of deeds

- County clerk

- Court clerk

- Property-tax office

- Secretary of State’s office

- Local land-records office

Office names and property-record systems vary by state and county, so start with the agency listed on the notice—but locate its contact information independently.

Look for the document or instrument number, recording date, filing party, amount claimed, property description, and any court case number. Save a complete copy, not just the first page.

This matters because a phrase like “claim against your property” can describe several very different situations.

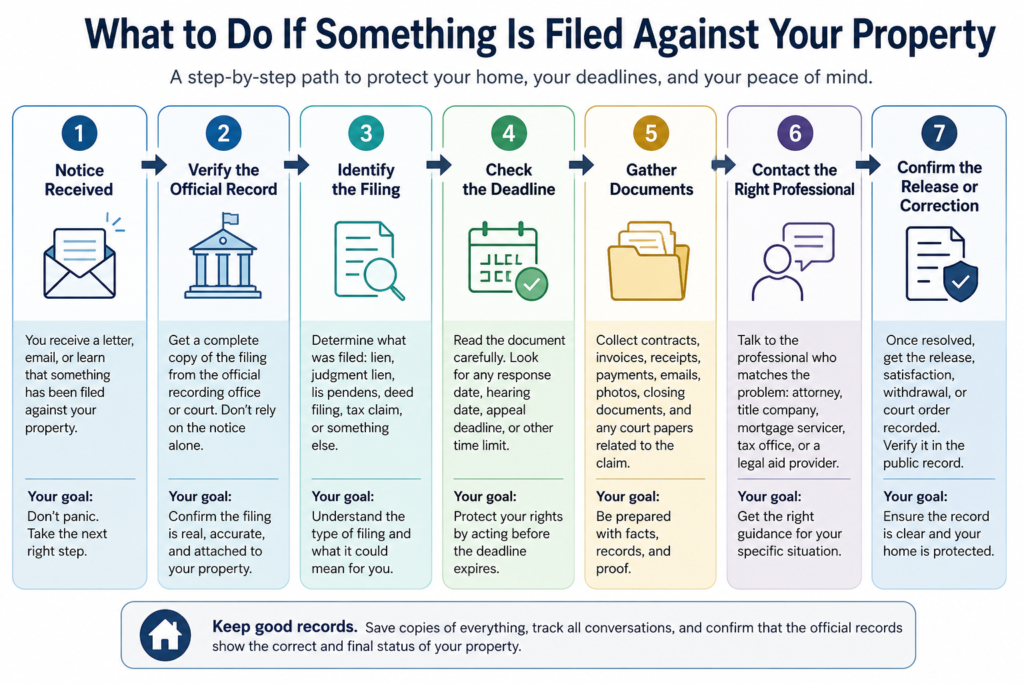

Property Defender: Start With the Record, Not the Worst-Case Scenario

Get the complete filing from the official recording or court office. Its title, date, filing party, document number, and deadline will tell you far more than an alarming letter or phone call.

Find Out What Was Filed Against Your Property

People often use the word “lien” as a catchall, but not every property filing is the same.

A lien is generally a legal claim connected to a debt or obligation. Depending on state law and the circumstances, liens may arise from unpaid taxes, contractor bills, court judgments, mortgages, homeowners association assessments, or other debts.

A judgment lien may result after a creditor wins a court judgment and takes the additional steps required under state law to attach it to real estate.

A lis pendens, sometimes called a notice of pending action, signals that a lawsuit may affect ownership of or an interest in the property. It isn’t necessarily a final judgment.

An ownership-related filing may involve a deed, transfer, mortgage, or other document that changes—or appears to change—the public record.

There may also be a less dramatic explanation. An old mortgage or other legitimate lien may have been paid, but the release was never recorded correctly.

Knowing which type of filing you’re dealing with changes everything that comes next.

A Filing Doesn’t Always Mean Someone Can Immediately Take Your Home

This is where legal language can make a stressful situation feel even worse.

A claim against property and the actual seizure or forced sale of property are not the same thing. A lien may give a creditor rights against the property, but additional legal steps are often required before a home can be sold or seized.

That doesn’t mean a lien is harmless.

A filing may interfere with a sale or refinance, affect who gets paid from the proceeds, create a title problem, or lead to further legal action. The consequences depend on the type of filing, the amount involved, its legal priority, and the laws in your state.

Think of the filing as a stop sign, not necessarily the end of the road. You need to pause, understand what’s there, and take the correct route forward.

Check the Names, Property Details, and Amount Carefully

Once you have the complete document, read it line by line.

Compare the filing against your own records. Look closely at:

- Your full legal name

- The property address

- Parcel or tax identification number

- Legal property description

- Filing party’s name

- Amount claimed

- Account, invoice, or case number

- Dates of work, service, judgment, or alleged nonpayment

- Signatures and notarizations, when applicable

Small discrepancies can matter.

The filing may belong to someone with a similar name, refer to the wrong parcel, list an amount you already paid, or relate to work you dispute. It may also be completely accurate.

Verification isn’t about looking for an excuse to dismiss the claim. It’s about making sure you respond to the right problem.

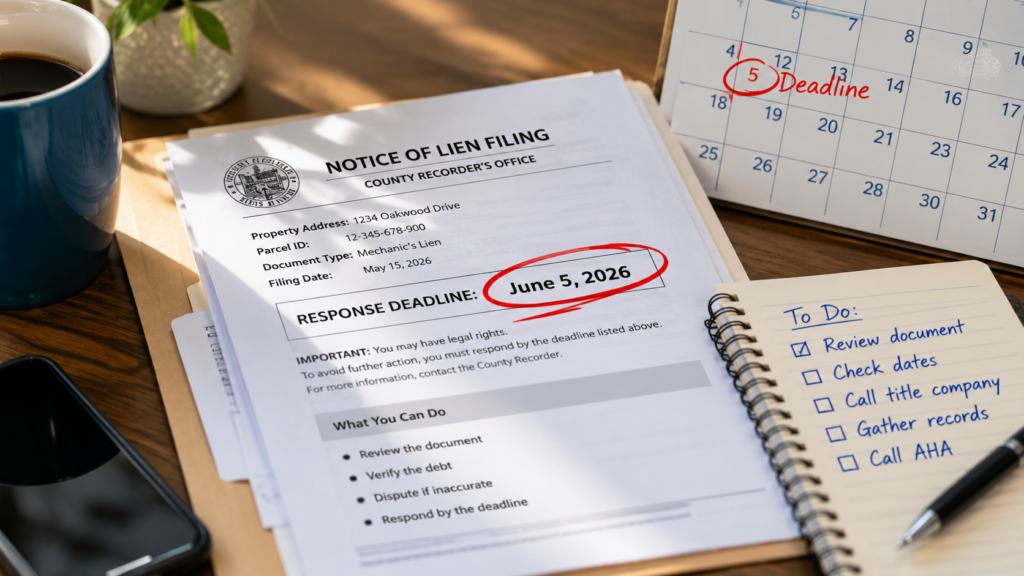

Look for a Deadline Before You Do Anything Else

Some property filings are primarily public records. Others are connected to a court case, tax proceeding, foreclosure process, or statutory dispute period.

That distinction can come with a clock.

If you received a summons, complaint, hearing notice, foreclosure document, or other court paper, read it carefully and identify the response date. Write it somewhere you’ll see it. Add it to your calendar. Take a picture. Tell anyone helping you about it.

Ignoring a court filing can allow the other party to move forward without your side of the story being heard.

And remember: calling the filing party usually doesn’t pause a legal deadline unless a court order, written agreement, or applicable law says otherwise.

Watch Out: A polite phone conversation isn’t a substitute for a required court filing. Treat any response, hearing, appeal, or foreclosure date as fixed until a qualified local professional confirms otherwise.

Preserve Your Records Before Contacting the Other Side

Unexpected property claims have a way of turning into scavenger hunts.

The contractor invoice is in one email account. The canceled check is buried in a banking portal. Your closing documents are in a box you haven’t opened since moving day.

Gather what you can before discussing the substance of the claim. Useful records may include:

- The notice and its envelope

- The complete recorded document

- Contracts, estimates, and change orders

- Invoices, receipts, and proof of payment

- Mortgage and closing documents

- Homeowners association statements

- Property-tax records

- Emails and text messages

- Photos of completed or disputed work

- Court papers

- Previous lien releases or satisfactions

Keep notes of every conversation, including the date, phone number, person’s name, and what was discussed.

Until you understand the filing, be cautious about admitting that you owe the money, agreeing to a payment plan, or signing a release or settlement. A rushed promise can make an already confusing situation harder to unwind.

Verify the Notice Independently

An official-looking letter isn’t proof that an official filing exists.

Don’t rely only on the phone number, website, or QR code printed on an unsolicited notice. Find the government office’s contact information independently and check the record there.

This is especially important when someone is selling a service that promises to “lock,” monitor, or instantly repair your title.

A real filing may exist alongside a misleading sales pitch. Verify both the document and the person offering to fix it.

What If the Filing Looks Fraudulent?

Seeing a deed or ownership document you didn’t sign can feel deeply unsettling.

Still, the basic order of operations remains the same:

- Preserve the document

- Verify it through the official land-records office

- Avoid signing anything

- Contact qualified help promptly

Depending on what was filed, your next calls may include:

- The county recorder or land-records office

- A local real-estate attorney

- Your title insurance company

- The title or settlement company from your purchase

- Your mortgage servicer

- Local law enforcement

- Your state attorney general or consumer-protection office

Some counties offer free property-record alerts that notify owners when a deed or other document is recorded under their name or parcel number. These alerts don’t prevent fraud, but they may help you spot a problem sooner.

Call the Professional Who Matches the Problem

“Talk to a professional” isn’t very useful advice when you don’t know which professional you need.

A real-estate attorney may be appropriate when ownership, title, foreclosure, or the validity of a lien is disputed.

A consumer-law or debt-defense attorney may be a better fit when the claim comes from a collection lawsuit or judgment.

A title company or title insurer may help when the filing relates to your purchase, an earlier owner, a covered title defect, or an unreleased lien.

Your mortgage servicer is the place to start when the issue involves your current loan, payment history, escrow account, or loan payoff.

The taxing authority should be contacted directly for property-tax claims.

A contractor-licensing agency, consumer-protection office, or construction attorney may be appropriate for a disputed contractor or mechanic’s lien.

A legal-aid organization may provide free or lower-cost assistance to homeowners who meet its eligibility requirements.

The recording office can usually tell you how to obtain a document and whether another document has been recorded. It generally can’t tell you whether the claim is legally valid or what defense you should raise.

Don’t Assume Paying Automatically Clears the Record

Suppose the claim is legitimate and you pay it.

Done, right?

Not always.

The underlying debt and the public record are related, but they may not be cleared in the same step. You may need a release, satisfaction, withdrawal, discharge, or court order—and that document may need to be recorded.

Before sending final payment, ask:

- Who will prepare the release?

- When will it be signed?

- Who will record it?

- Is a recording fee required?

- How will you receive a copy?

- How long should you wait before checking the public record?

Keep proof of payment and the recorded release with your permanent home documents.

How a Filing Can Affect a Sale or Refinance

Property claims often surface at the least convenient moment—usually when a title search is already underway.

A filing may delay closing, reduce the proceeds available to you, require money to be held in escrow, or prevent a lender or buyer from accepting clear title until the issue is resolved.

That doesn’t always mean the transaction is dead.

A title professional or attorney may be able to identify a payoff, release, correction, court procedure, or other path forward. But the earlier the issue is raised, the more room everyone has to work through it.

Once you know a filing exists, share it with the appropriate title, lending, and legal professionals early.

What Not to Do

A few reactions are understandable—but rarely helpful.

Set the notice aside and hope it goes away.

Even intimidating paperwork is easier to handle when you identify what it is and whether a deadline applies.

Treat the filing as automatically valid.

A recorded claim may still contain errors, relate to the wrong property, or reflect a debt you already paid.

Pay an unfamiliar company for an “instant” title fix.

Verify the filing and the company independently before sending money or sharing personal information.

Sign anything you don’t fully understand.

That includes deeds, settlements, releases, and payment agreements.

And don’t stop once someone says the problem is handled. Confirm that the appropriate corrective or release document appears in the official record.

Once It’s Resolved, Close the Loop

The last step is wonderfully unexciting: paperwork.

Obtain the final document that proves the matter was resolved. Depending on the situation, that may be a:

- Recorded lien release

- Satisfaction of judgment

- Withdrawal

- Corrective deed

- Court order

- Tax-lien release

- Payoff confirmation

- Title-company letter

Check the official records again after the expected processing period. Confirm that the release or correction is attached to the right property and document.

Then keep it.

Years from now, that one-page release may be the document that keeps a refinance or home sale from turning into another round of phone calls.

You Don’t Have to Solve Everything at Once

Finding out that something has been filed against your property is unsettling because the notice tends to arrive before the explanation.

Start smaller.

Get the document. Identify the filing. Check the deadline. Gather your records. Then bring the facts to the right person.

That sequence won’t make every lien or legal dispute simple. But it will help you avoid the two most expensive mistakes: ignoring a real problem and paying to fix a problem you haven’t verified.

Use the AHA Property Filing Worksheet to keep document numbers, deadlines, contact notes, and proof of resolution in one place. And explore AHA Property Defender for more tools that help you monitor and protect your home’s ownership records.

Property filings, deadlines, defenses, and removal procedures vary by state and local law. This article provides general homeowner information, not legal advice. Consider speaking with a qualified local attorney promptly when a filing involves a lawsuit, foreclosure, disputed ownership, suspected fraud, or a response deadline.