Buying a home comes with a lot of paperwork. Some of it feels familiar — mortgage, insurance, taxes. Then you hit the deed language.

Fee simple. Joint tenancy. Tenants in common. Tenancy by the entirety.

It’s the kind of language that makes a perfectly capable adult suddenly feel like they missed an entire semester of “how property works.” And honestly? That’s understandable. These terms aren’t everyday words, but they can affect very everyday things: who controls the home, who can sell it, what happens if someone dies, and whether adding a family member to the deed is a smart move or a future headache.

This guide breaks down the most common types of home ownership in plain English, so you know what your deed may be telling you — and when to pause before signing or changing anything.

This article is for general homeowner education, not legal, tax, or estate planning advice. Property ownership rules vary by state, and the exact wording on your deed matters.

Why Your Type of Home Ownership Matters

The way your home is titled can affect more than whose name appears on the deed.

It may influence:

- Who has the right to live in the home

- Who can sell, refinance, or transfer the property

- What happens when one owner dies

- Whether an owner’s share goes through probate

- How the home is treated during divorce, inheritance, or estate planning

- Whether a creditor may be able to reach an owner’s interest

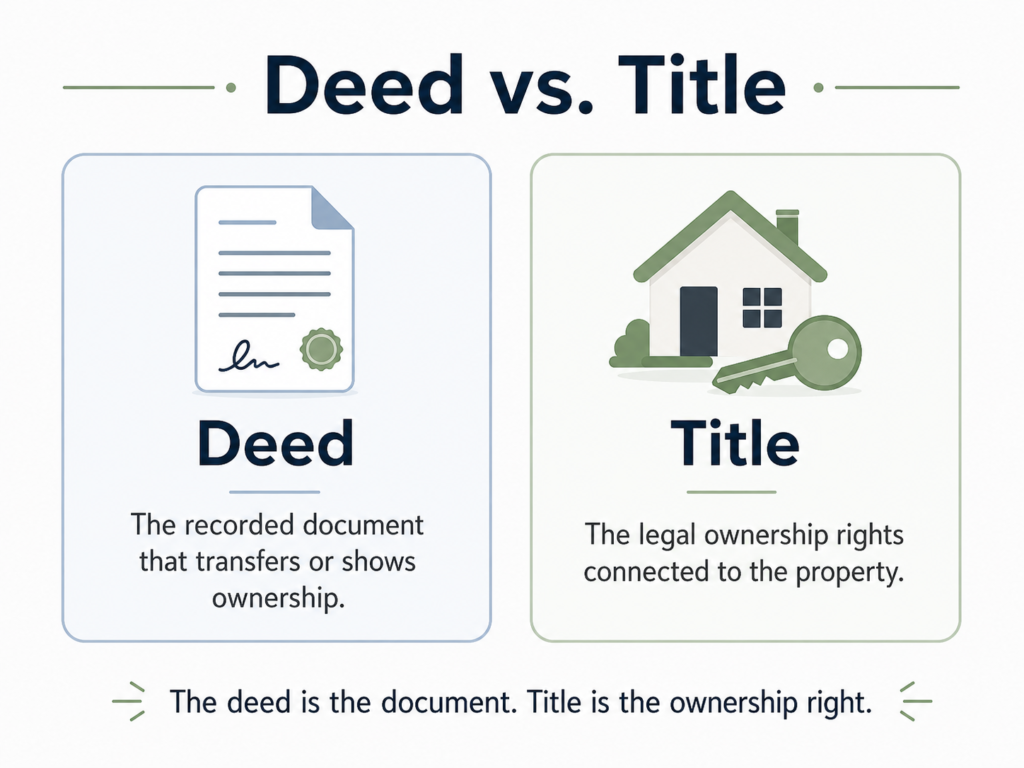

That sounds heavy because it is. A deed is not just a receipt for your house. It’s more like the instruction label attached to ownership.

And like most labels, you don’t want to read it for the first time during an emergency.

Fee Simple Ownership: The Standard “I Own My Home” Version

Fee simple ownership is the broadest and most common form of real estate ownership. Cornell’s Legal Information Institute describes fee simple as ownership that gives the owner the right to possess, use, and dispose of the property, and it can continue indefinitely.

For many homeowners, especially owners of detached single-family homes, this is the type of ownership they expect. You own the home and land, and you can generally sell it, leave it to heirs, refinance it, renovate it, or transfer it.

But fee simple does not mean “I can do absolutely anything I want.”

You may still be subject to:

- Your mortgage agreement

- Property taxes

- Zoning rules

- Building codes

- Easements

- Homeowners association rules

- Local ordinances

So yes, fee simple gives you strong ownership rights. But your home still lives inside a web of laws, contracts, and community rules.

Pro Tip: If you own a detached single-family home, your deed may say you own the property in fee simple. Still, don’t assume. Check your deed or title report and look at the exact language.

Sole Ownership: When One Person Owns the Home

Sole ownership means one person owns the property in their name alone.

This can happen when someone buys a home before marriage, inherits a property individually, or chooses to keep title in one person’s name.

On paper, sole ownership is simple. In real life, it can get complicated.

For example, if the sole owner dies, the home may need to go through probate unless there is another legal arrangement in place, such as a trust or a transfer-on-death deed where allowed. If the owner marries, divorces, refinances, or uses marital funds to improve the home, state law may affect how the property is treated.

That’s where homeowners can get surprised. The deed may say one thing. Family law, tax law, estate planning, or state property rules may add another layer.

Watch Out: Adding someone to your deed “just to make things easier” can create tax, inheritance, creditor, divorce, or control issues. It may feel like a small paperwork change. It usually isn’t.

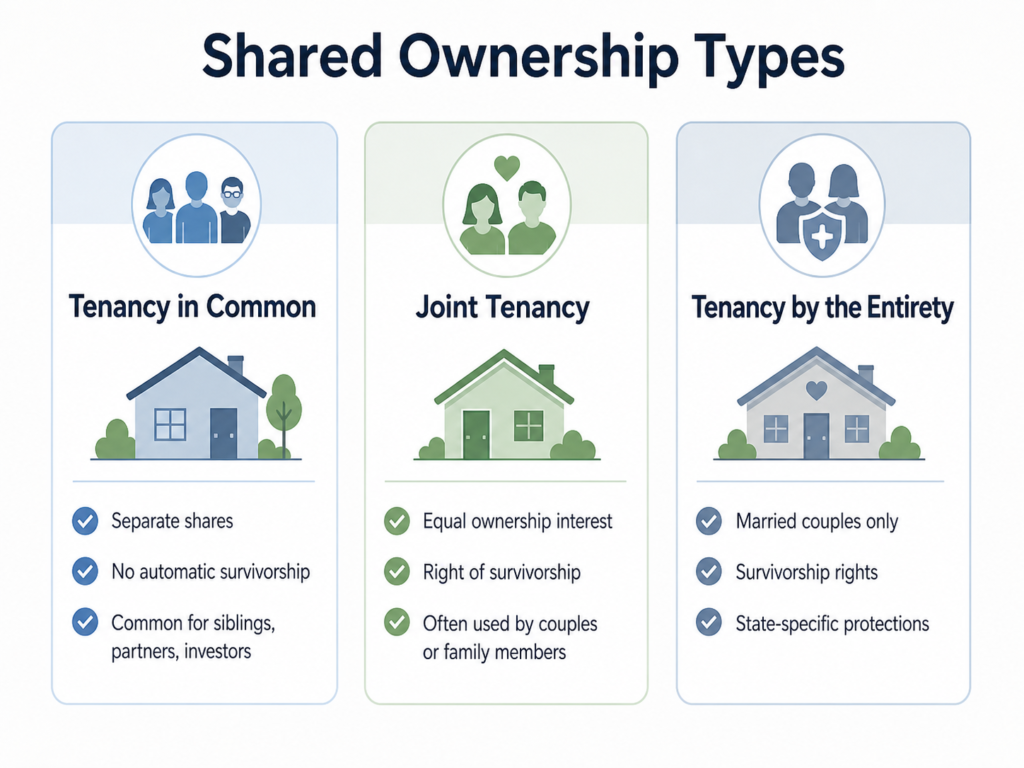

Tenancy in Common: Shared Ownership With Separate Shares

Tenancy in common means two or more people own the same property, but each person owns a separate share. Those shares can be equal or unequal. Cornell describes tenancy in common as a form of concurrent ownership where each owner has a fractional interest and the right to possess the whole property.

That last part surprises people.

Even if one person owns 25% and another owns 75%, both may have the right to use the entire property unless a separate agreement says otherwise.

Tenancy in common often shows up when:

- Siblings inherit a home together

- Unmarried partners buy a house

- Friends purchase property jointly

- Investors buy a rental property

- Family members hold different ownership percentages

The big thing to understand: in many cases, a tenant in common’s share does not automatically go to the other owners when that person dies. Instead, that share may pass through the person’s will, trust, or state inheritance law.

That can be perfectly fine when everyone plans for it.

It can also turn into a mess. Picture three siblings inheriting a lake house, then one sibling’s share passes to two adult children who don’t agree on whether to keep it, rent it, or sell it. Suddenly the “family place” has a spreadsheet, a group text, and hurt feelings.

Joint Tenancy: Shared Ownership With Survivorship Rights

Joint tenancy is another form of shared ownership. Its defining feature is usually the right of survivorship. Cornell explains that joint tenants each have an undivided interest in the property, and when one joint tenant dies, that person’s interest passes to the surviving joint tenant or tenants.

In plain English: if two people own a home as joint tenants with right of survivorship, and one dies, the surviving owner typically becomes the full owner automatically.

That can be useful for married couples, partners, or family members who want the home to pass without waiting for probate.

But joint tenancy is not just an estate-planning shortcut. It usually gives the other person ownership rights now, not later.

That means adding someone as a joint tenant may affect:

- Your ability to sell or refinance

- Exposure to the other owner’s creditors

- Divorce or separation issues

- Family inheritance plans

- Control of the property

Pro Tip: Before adding an adult child, partner, or relative as a joint tenant, ask: “What rights am I giving them today?” Not just, “What happens when I’m gone?”

Tenancy by the Entirety: A Married-Couple Ownership Form

Tenancy by the entirety is a special type of ownership available to married couples in many states. Cornell describes it as a form of concurrent ownership between spouses that includes survivorship rights and generally prevents one spouse from transferring their interest without the other spouse’s consent.

In some states, tenancy by the entirety may also provide protection from creditors of only one spouse. Cornell notes that, in many jurisdictions, creditors of one spouse alone may not be able to attach property held by the entirety.

That can be a meaningful protection. But this is one of those areas where state law matters a lot.

Some states recognize tenancy by the entirety. Some don’t. Some apply it only to real estate. Some may treat creditor issues differently.

If you’re married and buying a home, this is a good question to raise before closing:

“Should we take title as joint tenants, tenants by the entirety, community property, or something else under our state’s law?”

Not exactly romantic dinner conversation. But useful.

Community Property: A Different System for Some Married Homeowners

In community property states, property and income acquired during marriage may be treated as jointly owned by both spouses, depending on state law and how the property is classified.

The IRS says community property laws affect how married taxpayers in community property states figure income on federal tax returns, and Publication 555 identifies Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin as community property states.

Community property can affect taxes, divorce, inheritance, and estate planning. It can also matter if you move from one state to another.

For example, a couple may buy a home in California, move to Colorado, then later update their estate plan. The old assumptions may not fit the new situation.

This is why title and estate planning should be reviewed after major life changes. Marriage, divorce, death of a spouse, relocation, inheritance, and refinancing can all change the picture.

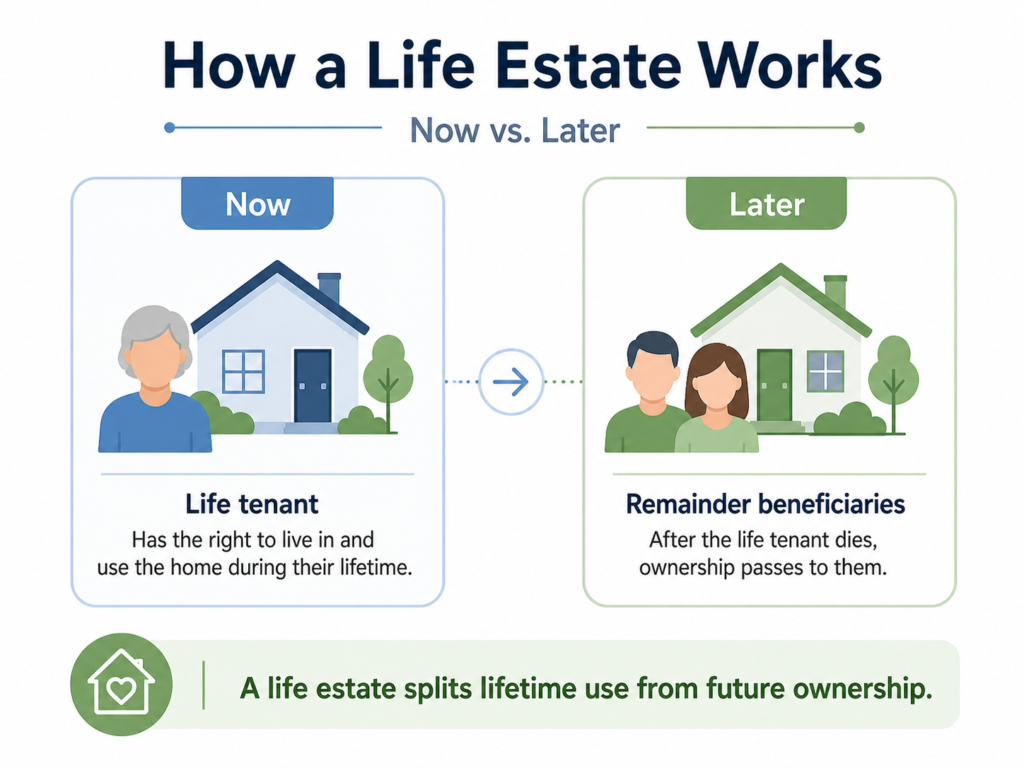

Life Estate: The Right to Use a Home During a Lifetime

A life estate gives one person the right to use or live in a property during their lifetime. That person is often called the life tenant. When the life tenant dies, the property passes to another person or group, often called the remainder beneficiaries.

This sometimes comes up in estate planning. For example, a parent may transfer a home to adult children while keeping the right to live there for the rest of their life.

That can sound neat and tidy. Sometimes it is.

But a life estate can also make things harder. Selling or refinancing the home may require cooperation from multiple people. The life tenant and future owners may have different priorities. Repairs, taxes, insurance, and upkeep need to be clearly understood.

A life estate is like building a bridge between today’s ownership and tomorrow’s inheritance. If the bridge is built carefully, it can help. If it’s built casually, everyone may end up stuck in the middle.

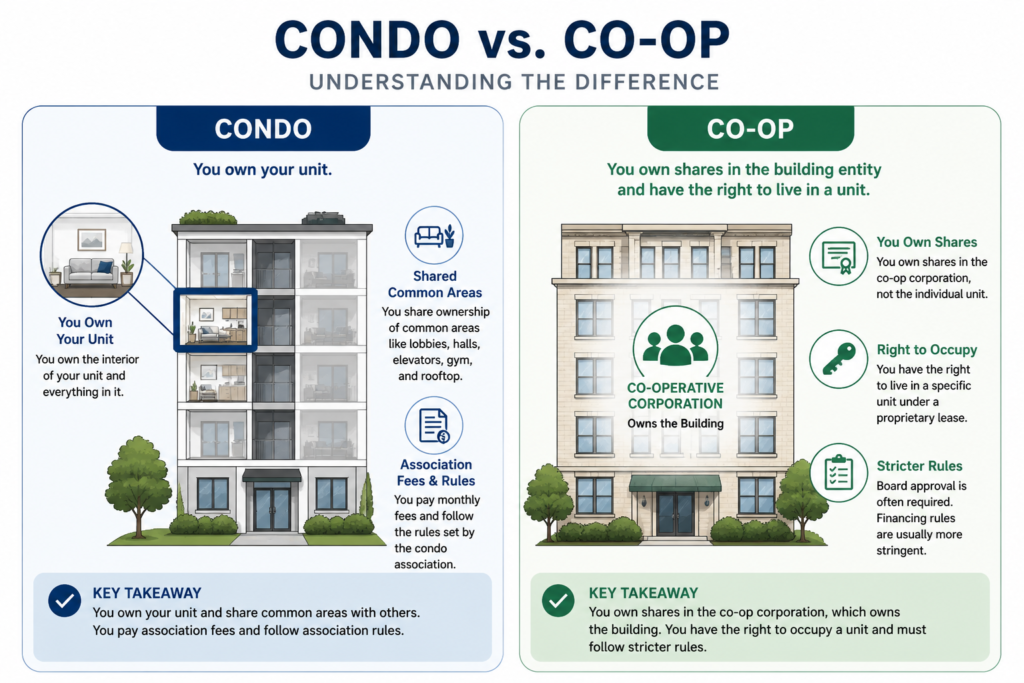

Condo Ownership: You Own the Unit, Share the Rest

With a condominium, you typically own your individual unit and share ownership or responsibility for common areas.

That may include:

- Roofs

- Hallways

- Elevators

- Parking areas

- Landscaping

- Exterior walls

- Amenities

A condo can be a great fit if you want less exterior maintenance. But you are also buying into a shared system.

That means association fees, rules, reserve funds, insurance issues, and special assessments matter. A low monthly fee can look nice today, but if the association hasn’t saved enough for a roof, elevator, or structural repair, owners may face a large special assessment later.

Watch Out: When buying a condo, review the association documents, budget, reserves, insurance coverage, recent meeting minutes, and any pending special assessments. The unit matters. The building’s financial health matters too.

Co-op Ownership: You Own Shares, Not the Unit Itself

A cooperative, or co-op, is different from a condo.

With a condo, you typically receive a deed to your unit. With a co-op, a corporation or cooperative usually owns the building, and residents own shares or membership interests that give them the right to occupy a particular unit.

Fannie Mae describes a cooperative as a property where shareholders or equity owners are granted the right to occupy a unit under a proprietary lease or occupancy agreement.

That difference matters.

Co-ops may have stricter rules around:

- Board approval

- Financing

- Subletting

- Renovations

- Selling shares

- Occupancy requirements

Co-ops can work beautifully for the right homeowner, especially in cities where they’re common. But they are not the same as owning a single-family home or a condo. You’ll want to understand the rules before falling in love with the apartment.

Trust Ownership: When a Trust Holds Title

Sometimes a home is owned by a trust.

This is common in estate planning. A homeowner may place property into a revocable living trust so the home can be managed more smoothly if they become incapacitated and may avoid probate when they die.

Trust ownership is not a physical housing type. You can have a single-family home, condo, vacation home, or rental property held in a trust.

The key is coordination. The deed, trust document, mortgage, insurance policy, and estate plan should all line up. If one piece is out of sync, the trust may not work the way the homeowner expected.

Quick Comparison of Common Home Ownership Types

| Ownership Type | Plain-English Meaning | Common Use | Key Thing to Watch |

|---|---|---|---|

| Fee Simple | Broadest standard ownership rights | Single-family homes | Still subject to taxes, zoning, liens, easements, and homeowners association rules |

| Sole Ownership | One person owns the property | Individual buyers, inherited homes | Probate, marriage, divorce, and estate planning issues |

| Tenancy in Common | Multiple owners hold separate shares | Siblings, partners, friends, investors | One owner’s share may pass to heirs, not the other owners |

| Joint Tenancy | Shared ownership with survivorship rights | Couples, family members | Adding someone gives them ownership rights now |

| Tenancy by the Entirety | Married-couple ownership in many states | Married homeowners | State rules and creditor protections vary |

| Community Property | State-law marital property system | Married couples in community property states | Tax, divorce, and inheritance consequences |

| Life Estate | Right to use property for life | Estate planning | Sale or refinance can be complicated |

| Condo | Own unit, share common areas | Multifamily buildings, townhomes | Association rules, fees, reserves, and special assessments |

| Co-op | Own shares plus occupancy rights | Urban apartment-style housing | Board approval and financing rules |

| Trust Ownership | Trust holds title | Estate planning | Documents, insurance, and lender rules must align |

How to Find Out What Type of Ownership You Have

Start with your deed.

Depending on your state, it may be called a warranty deed, grant deed, quitclaim deed, special warranty deed, trustee’s deed, or something similar.

Look for the owner names and the wording that follows them. You may see phrases such as:

- “as tenants in common”

- “as joint tenants with right of survivorship”

- “as tenants by the entirety”

- “as community property”

- “as trustee of the Smith Family Trust”

- “in fee simple”

You can usually get a recorded copy of your deed from your county recorder, register of deeds, clerk, or land records office. Your title company, closing attorney, or real estate attorney may also have a copy from when you bought or refinanced the home.

If you don’t understand the wording, don’t guess. Deed language is one of those places where a few words can carry a lot of weight.

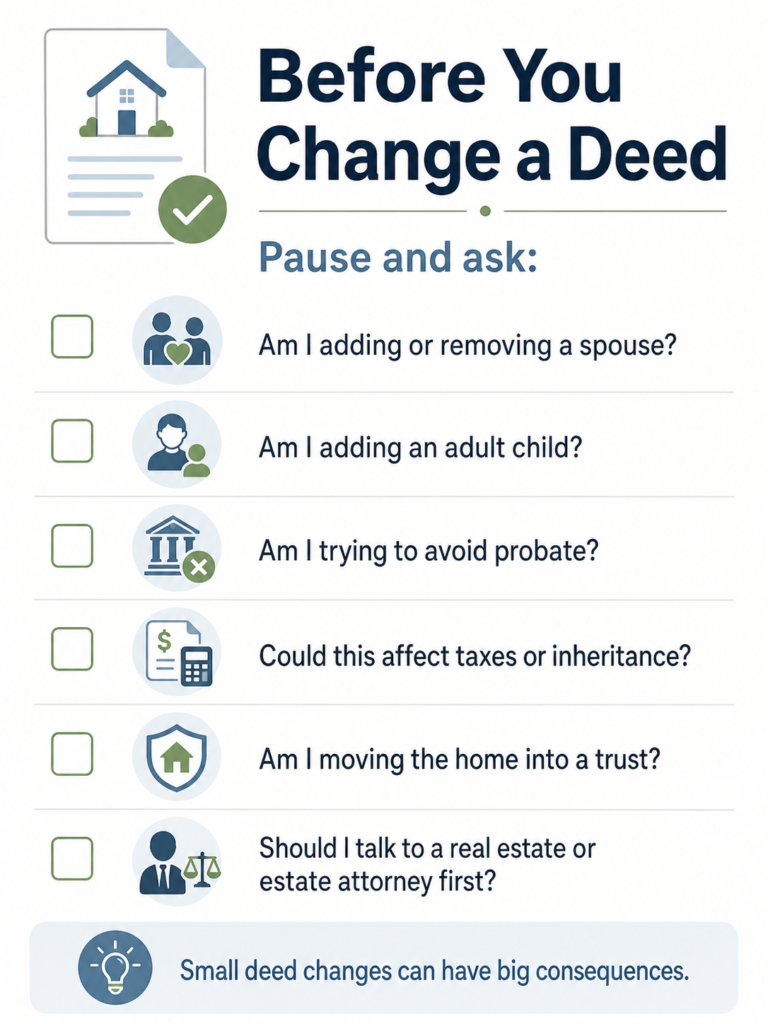

When to Ask a Professional Before Changing a Deed

You should consider talking with a real estate attorney, estate planning attorney, title company, or tax professional before changing ownership if:

- You’re adding or removing a spouse

- You’re adding an adult child to the deed

- You’re buying with an unmarried partner

- You inherited a home with siblings or relatives

- You’re trying to avoid probate

- You’re moving a home into or out of a trust

- You’re worried about creditors, divorce, Medicaid, or taxes

- You own property in more than one state

- You recently moved from a community property state

- You’re refinancing and title language is changing

This is not about making the process scarier. It’s about preventing one of the most frustrating homeowner problems: trying to undo a document that was recorded too casually.

The Bottom Line

You don’t need to become a property lawyer to be a smart homeowner.

But you do need to know that deed language matters.

The type of home ownership can affect who controls the property, who inherits it, who can sell it, and what happens when life changes. And life does change — marriage, divorce, aging parents, adult children, inheritance, refinancing, moving states. The house may stay put, but your legal situation may not.

So take the practical next step: review your deed, save a copy with your important home documents, and ask for help before changing title.

AHA helps homeowners reduce the cost and complexity of homeownership with plain-English guidance, tools, and checklists that make the paperwork side of owning a home feel a little less overwhelming.