Learning how to plan for major home repairs can make homeownership feel a lot less chaotic.

Most homeowners understand, at least in the back of their minds, that a house won’t stay exactly the same forever. Roofs weather. Mechanical systems wear down. Water heaters age slowly from the inside out. Nothing dramatic may happen for years, and then one day a quote lands in your inbox: five figures for a roof, four figures for a water heater, or a repair bill that feels sudden even though the system had been aging for decades.

That’s the part that catches people off guard.

Major home repairs usually don’t feel stressful simply because they’re expensive. They feel stressful because they arrive without enough orientation. Most homeowners are given maintenance checklists, emergency fund advice, and broad rules of thumb like “save 1% of your home’s value.” Those ideas can help, but they don’t explain the rhythm of a home.

And homes do have a rhythm.

Once you recognize that pattern, major repairs stop feeling like financial ambushes. They start looking more like lifecycle transitions — and transitions can be planned for.

The Blind Spot Most Homeowners Carry

When you bought your home, the affordability picture was probably reviewed from every angle. Your lender focused on the monthly payment, your agent walked you through market value, and your inspector looked for visible defects or immediate concerns.

What most homeowners don’t receive is a long-term aging map of the house itself.

That missing context matters. Major repairs are rarely random events. More often, they’re systems reaching maturity. But without lifecycle awareness, maturity can feel like malfunction.

A 22-year-old roof approaching the end of its useful life is not automatically a crisis. It may simply be a cycle completing itself. Still, if no one has helped you understand that cycle, the repair can feel like something went wrong.

That mental shift — from “something failed” to “this system reached its next phase” — is subtle, but it can make homeownership feel much steadier.

Your Home Is a Collection of Timelines

One of the most helpful ways to think about your home is to stop seeing it as one single thing.

Your home is really a collection of systems, and each one is aging on its own timeline. The roof has its arc. The HVAC system has its arc. The water heater, plumbing lines, electrical infrastructure, windows, siding, appliances, drainage, and exterior finishes are all moving quietly through time.

When you see your home as a portfolio of timelines rather than one static asset, aging becomes easier to notice. And once aging becomes visible, it becomes much easier to manage.

Seasoned Advice: Homes don’t suddenly become expensive. They move through phases. Stress often begins when homeowners don’t recognize which phase they’ve entered.

Maintenance Is Not the Same as Planning

Maintenance is responsible, and it matters. Servicing your HVAC system, clearing gutters, sealing windows, checking caulk, replacing filters, and keeping up with small repairs can all extend performance and reduce avoidable problems.

But maintenance does not stop time.

A well-maintained furnace can still reach the end of its internal lifespan. A carefully inspected roof can still cycle out. Materials fatigue, components wear, and systems eventually need replacement even when you’ve taken good care of them.

That’s why maintenance and planning serve two different purposes. Maintenance helps your home perform better today. Planning helps you prepare for what your home will likely need tomorrow.

If you want to understand how to plan for major home repairs in a practical way, separating those two ideas is foundational.

The Comfort — and Limits — of the 1% Rule

You’ve probably heard the advice to save 1% to 4% of your home’s value each year for maintenance and repairs. As a starting point, that rule isn’t unreasonable. It creates forward motion, and forward motion is useful.

The problem is that a percentage rule lacks context.

That rule doesn’t tell you whether your roof is five years old or twenty-two. It also can’t show you if several major systems were installed around the same time, or whether climate, storm exposure, installation quality, material grade, or a previous owner’s deferred maintenance may shorten the timeline.

Rules of thumb are averages. Lifecycle awareness is more specific.

Seasoned Advice: Rules of thumb are helpful when you don’t yet know your systems. Once you do, the conversation becomes calmer — and more precise.

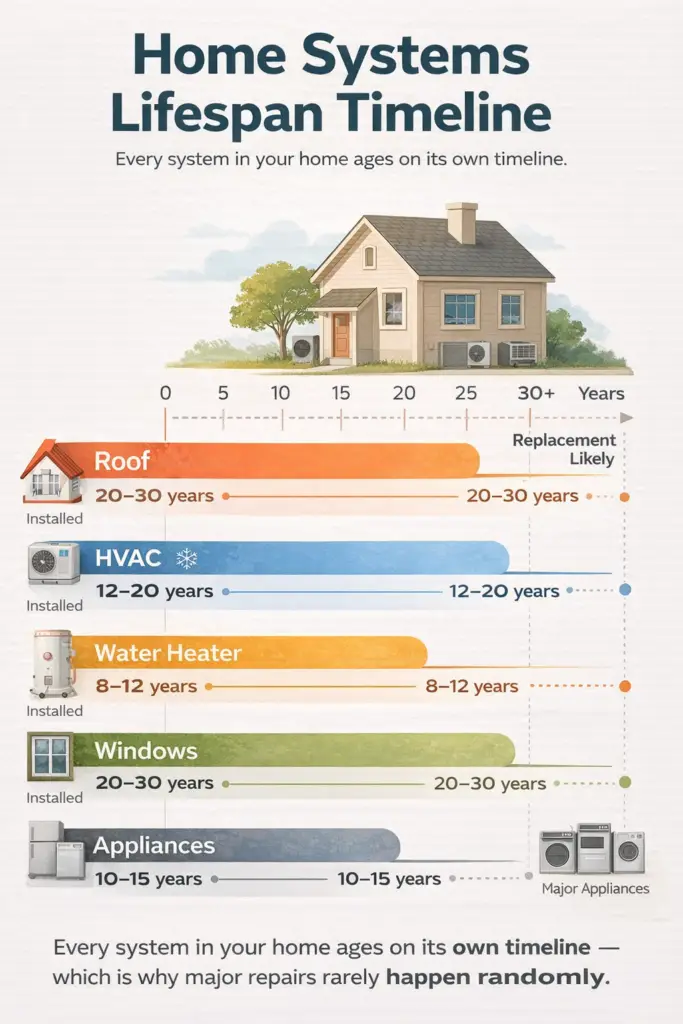

Typical Planning Ranges for Major Home Systems

You don’t need perfect numbers to start planning. You just need rough orientation.

The ranges below are general planning guides, not guarantees. Your actual timeline can shift based on climate, installation quality, maintenance history, usage, material type, and local conditions.

| Home System | Common Planning Range |

|---|---|

| Asphalt shingle roof | 20–30 years |

| HVAC system | 12–20 years |

| Water heater | 8–12 years |

| Exterior paint or stain | 5–10 years |

| Windows | 20–30+ years |

| Siding | Varies widely by material |

| Major appliances | 8–15 years |

| Electrical panel | Often long-lasting, but may need upgrades as household demand changes |

| Plumbing lines | Varies widely by material, age, and water quality |

Watch Out: These ranges are not replacement deadlines. They’re planning signals. A 16-year-old HVAC system may run for years, or it may need replacement sooner than expected. The goal isn’t to predict the exact failure date. It’s to avoid being financially surprised when the system enters its later stage.

Planning Bands, Not Predictions

You do not need to predict the exact year a system will fail. That’s usually impossible, and trying to do it can create more anxiety than clarity.

Instead, think in planning bands.

A planning band is a window of time when replacement becomes increasingly likely. It is not a guarantee, and it does not mean you need to rush into a project. It simply means the system is getting older and deserves more attention in your financial planning.

For example, if your HVAC system is nearing the upper end of its typical lifespan, that does not have to be a warning siren. It can simply be a signal to prepare gradually. The same idea applies to roofs, water heaters, exterior finishes, and other major systems.

Awareness gives you space. And space gives you options. You can gather bids, evaluate materials, ask better questions, and adjust your savings rhythm before urgency takes over.

AHA Pro Tip: When a system enters its planning band, request estimates even if you’re not ready to replace it. Pricing clarity removes anxiety and helps prevent rushed decisions later.

Forecasting is not about certainty. It’s about narrowing the range of surprise.

How to Build Your Home Repair Planning Map

This is where repair planning becomes useful in real life.

You don’t need a complicated spreadsheet or a perfect record of every past repair. A simple table, notebook, or home binder is enough to get started. The goal is to create a basic map of your home’s major systems so you can see what may be coming.

Start with four columns:

| System | Approximate Age | Planning Status | Notes |

|---|---|---|---|

| Roof | 18 years | Start planning | Get 2–3 estimates within the next year |

| HVAC | 12 years | Watch closely | Schedule service and ask about expected remaining life |

| Water heater | 9 years | Near planning band | Check warranty and installation date |

| Electrical panel | Unknown | Verify | Ask electrician during next service visit |

| Windows | 22 years | Monitor | Note drafts, condensation, or failed seals |

| Siding | 15 years | Monitor | Check for rot, cracking, gaps, or moisture issues |

Begin with the big three: your roof, HVAC system, and water heater. Those systems alone can tell you a lot about your next five to ten years of ownership.

From there, add other systems as you learn more. Look for installation stickers, review inspection reports, check permit records if your local building department makes them available, and ask contractors to note approximate ages during routine service calls.

You don’t need perfect information. You just need enough orientation to stop flying blind.

Why Major Repairs Often Arrive in Waves

Here’s where many homeowners feel blindsided: cluster risk.

Homes are typically built with multiple systems installed around the same time. That means those systems often age together. If your roof, HVAC system, water heater, and appliances were all installed when the home was built, they may not fail in the same month or even the same year, but they may enter their replacement windows within the same five-year stretch.

Consider a home built in 2006 with many original systems. By 2023–2028, the roof may be entering its later stage, the HVAC system may be approaching replacement, the water heater may already have cycled out, and some appliances may be on borrowed time.

Nothing unusual has happened. No disaster. Just time.

Individually, each repair might be manageable. But when several systems age into replacement range close together, the costs compress. Without awareness, that compression feels chaotic. With awareness, it becomes something you can schedule around.

You might decide to replace one system slightly early to spread out the financial impact. You may also increase savings during a known cluster window, gather pricing before the work becomes urgent, or prioritize one system now while allowing another to wait.

Seasoned Advice: Cluster risk is rarely misfortune. It’s often original construction timing revealing itself later.

We’ve seen homeowners refinance under pressure for a roof that was predictable years earlier. The cost wasn’t the only problem. The compression was.

Timing Is Leverage

Emergency replacements narrow your options.

When a system fails suddenly, your ability to compare bids, check reviews, verify credentials, and evaluate materials shrinks quickly. Urgency can limit your choices and make it harder to compare pricing with a clear head.

When you choose timing instead of reacting to it, you regain leverage. You can decide when to gather estimates, whether to repair or replace, which materials make sense, and whether the project fits better in one season than another.

AHA Pro Tip: HVAC installations may be easier to schedule during spring and fall shoulder seasons in some markets. Roofing and exterior projects may also be more flexible outside peak demand periods, depending on your local climate.

When urgency drops, leverage rises. Understanding how to plan for major home repairs gives you that leverage.

Capital Reserves Are Not Emergency Funds

An emergency fund protects against unpredictable life events. Major system aging is different. It may not be perfectly predictable, but it is cyclical.

If you rely only on emergency savings for predictable home replacements, you blur two very different financial jobs. A separate home repair reserve creates steadiness because it gives future repairs a place to live in your budget before they become urgent.

That does not mean every homeowner needs a large dedicated account overnight. Start where you are. Even a small monthly amount assigned to future repairs can change the way you feel about your home.

There is no single correct planning style. Some homeowners prefer conservative pacing with larger reserves. Others take a moderate approach and adjust gradually. Some smooth cluster risk through project timing, financing strategy, or planned savings increases.

What matters is intentionality.

Seasoned Advice: Financial calm comes from rhythm, not reactive swings.

What to Do When You Can’t Fully Fund Every Repair

Let’s be honest: not every homeowner can easily set aside thousands of dollars for future repairs. That does not mean planning is pointless.

Planning still helps because it gives you time to make better decisions.

If a major system is entering its planning band and your savings are not where you want them to be, start with realistic pricing. Guessing is usually more stressful than knowing. Then prioritize safety and damage prevention. A failing roof, unsafe electrical issue, or leaking water heater deserves a different level of attention than a cosmetic upgrade.

Finally, explore your options before urgency takes over. Depending on the project, that might mean savings adjustments, vetted financing, local assistance programs, rebates for energy-related upgrades, or timing the work during a less expensive season.

Watch Out: Don’t wait until a system fails to learn what replacement costs in your area. The first estimate you see during an emergency can feel like the only option — even when it isn’t.

Planning does not require wealth. It requires visibility. And visibility gives you choices.

Insurance, Equity, and Selling — Viewed Differently

Lifecycle awareness influences decisions beyond repairs.

When you understand where your roof sits in its lifecycle, insurance conversations become clearer. Normal wear and tear usually is not covered by homeowners insurance, though sudden damage related to a covered event may be handled differently depending on your policy, deductible, state rules, and insurer. That’s why it helps to read your policy before you need it.

Cluster windows also make refinancing decisions calmer. Borrowing under pressure is expensive. Borrowing with foresight is optional.

If you’re preparing to sell, aging systems become negotiation variables rather than surprises. A buyer may accept an older HVAC system if the service records are clear. They may feel better about an aging roof if there is documentation, recent inspection information, or transparent pricing.

Uncertainty creates friction. Documentation reduces it.

AHA Pro Tip: Keep installation dates, service records, permits, warranties, inspection reports, and contractor invoices organized. Buyers and insurers often fear uncertainty more than aging.

Capital awareness improves positioning.

Where Even Thoughtful Homeowners Get Caught

Even diligent homeowners can get caught by gradual aging.

Many homeowners anchor to past pricing, assuming a roof that cost $12,000 fifteen years ago will feel similar today. Others maintain systems carefully and assume replacement is still far off, or they look at each repair in isolation instead of noticing how several systems may be aging together.

None of this reflects irresponsibility. It reflects how people process slow change.

We respond to urgency. Homes age gradually. Without a framework, gradual aging can become urgent all at once. With a framework, it becomes paced.

A Simple Annual Home Repair Planning Routine

Once a year, give your home a quiet financial check-in.

This does not need to become a stressful clipboard-and-hard-hat production. It can be a simple review at the start of the year, around tax time, or during seasonal maintenance.

Ask yourself which systems are getting older, which repairs you’ve been delaying, and which replacement would be most disruptive if it happened suddenly. Then consider which project you should price this year, even if you don’t schedule it yet, and what documentation you’re missing.

The point is not to obsess over your house. The point is to stay oriented.

The Real Objective

You cannot eliminate major home repair costs. What you can reduce is the shock.

You don’t need perfect projections. You need orientation. Specifically, you need to know which systems are still early in their lifecycle, which are entering planning bands, and whether clustering is forming.

From there, ownership steadies. Savings feel more purposeful. Decisions feel more measured. Contractor conversations feel less rushed. Insurance and selling decisions become clearer.

Homes age. That’s normal. What changes everything is whether that aging feels chaotic or scheduled.

When you understand how to plan for major home repairs with lifecycle awareness instead of guesswork, you do not eliminate cost. You eliminate some of the surprise, and that is often the difference between stress and stability.

Frequently Asked Questions About Planning for Major Home Repairs

How much should I save for major home repairs?

A common starting point is 1%–4% of your home’s value annually for maintenance and repairs. However, system-based planning is usually more useful because it accounts for your home’s actual age, materials, climate, and repair history.

What qualifies as a major home repair?

Major repairs typically involve full system replacement or substantial work, such as roof replacement, HVAC replacement, plumbing line updates, electrical panel upgrades, foundation repairs, structural work, or major exterior repairs.

Does homeowners insurance cover aging systems?

Homeowners insurance generally does not cover normal wear and tear or end-of-life replacement. It may cover sudden and accidental damage caused by a covered event, depending on your policy and circumstances. Review your policy or ask your insurance professional before assuming something is covered.

How do I know when to replace my roof or HVAC system?

Rather than trying to predict an exact year, identify a planning band near the upper end of the system’s expected lifespan. Once a system enters that window, start gathering information, pricing, and professional opinions.

What is cluster risk?

Cluster risk happens when multiple major systems approach replacement within the same few years because they were installed around the same time. This is common in homes where many original systems are still in place.

Is a capital reserve different from an emergency fund?

Yes. A capital reserve prepares for predictable home system aging. An emergency fund protects against unexpected life disruptions, such as job loss, medical bills, or urgent family needs.

What should I check first if I’m new to home repair planning?

Start with your roof, HVAC system, and water heater. Find their approximate ages, check service records, and note whether any are entering a likely planning window.

Final Takeaway

Major repairs feel less overwhelming when you stop treating them as surprises and start seeing them as part of your home’s lifecycle.

You don’t need to know the exact month your roof, HVAC system, or water heater will fail. You just need enough visibility to prepare before urgency takes over.

Start by finding the age of your roof, HVAC system, and water heater. Then build a simple repair planning map around those systems.

That’s the quieter side of smart homeownership: not panic, not perfection, just rhythm.

Explore more AHA homeowner tools to help plan repairs, organize home records, and reduce the cost and complexity of owning your home.