It usually doesn’t start with a plan.

It starts with a quiet what if.

What if your income changes?

What if retirement comes sooner than expected?

What if your home—the biggest asset you’ve built—could help carry the load?

That’s when reverse mortgages enter the conversation.

On paper, they sound simple: no monthly payments, access to your equity, more breathing room.

But here’s the part most homeowners don’t hear upfront…

A reverse mortgage isn’t a quick fix. It’s a long-term decision that trades future flexibility for present relief.

If you’re thinking about using your home as a safety net, this will help you understand what that really means—and whether it’s the right move.

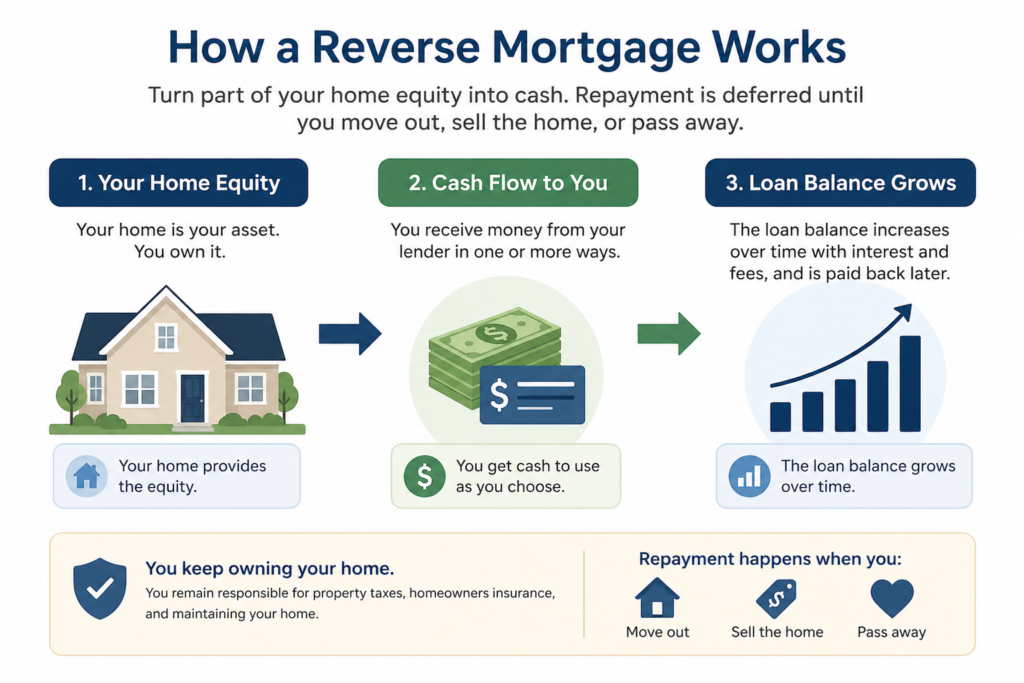

What Is a Reverse Mortgage and How Does It Work?

A reverse mortgage lets you borrow against your home equity without making monthly mortgage payments.

Instead, the loan balance grows over time.

You’re essentially using your home’s value now… and repaying it later—usually when:

- You sell the home

- You move out permanently

- Or the last borrower passes away

Most reverse mortgages in the U.S. are Home Equity Conversion Mortgages (HECMs), which are federally insured and available to homeowners age 62 and older.

What Are the Hidden Costs of a Reverse Mortgage?

This is where things get real.

Even without a monthly mortgage payment, you’re still responsible for:

Those don’t go away.

And if they fall behind, you can still risk foreclosure.

A reverse mortgage doesn’t remove the cost of owning a home—it only removes one payment.

That’s something experienced pros consistently emphasize: homeownership always comes with ongoing responsibility, no matter how it’s financed

Reverse Mortgage Pros (When It Can Help)

There are situations where this tool genuinely works—and it’s important to be clear about that.

✔️ It can remove your largest monthly stress point

If your mortgage payment is what’s tightening your budget, eliminating it can create immediate breathing room.

For some homeowners, that’s the difference between constant financial pressure and a manageable plan.

✔️ It can support fixed retirement income

If most of your income is predictable—like Social Security, a pension, or disability—a reverse mortgage can act as a buffer rather than your primary source.

✔️ It allows you to stay in your home

If your goal is to age in place, this can help you stay put without selling or downsizing.

Reverse Mortgage Cons (What You’re Really Trading Away)

This is where most homeowners wish they had slowed down.

❗ The loan balance grows over time

Interest compounds on what you borrow.

That means:

- Less equity later

- Smaller inheritance for your family

❗ It’s one of the more expensive ways to access equity

Between fees, mortgage insurance, and interest, reverse mortgages are not a low-cost option.

❗ It limits your flexibility later

If you decide to move, downsize, or relocate, the loan comes due.

That can force decisions on a timeline you didn’t expect.

❗ It’s easy to use it too early

This is the most common mistake.

A reverse mortgage is designed as a later-stage tool…

…but it often gets used as a first move during uncertainty.

The Real Question: Is This an Income Problem or an Equity Decision?

This is where most advice goes sideways.

If you’re considering a reverse mortgage because your income might change…

You’re not really solving a home equity problem.

You’re trying to solve a financial stability problem.

And those should be handled differently.

👉 Not sure which situation you’re actually in?

Use the AHA “Should I Use My Home Equity?” checklist to slow this down and think it through before making a big decision.

What Are Alternatives to a Reverse Mortgage?

Before turning your home into a funding source, start with options that keep you flexible.

1. Map your “worst-case” monthly budget

Not your current lifestyle—your bare minimum.

You might find your situation is more stable than it feels.

2. Stretch your savings strategically

Instead of asking “Do I have enough?” try:

“How many months can I buy myself?”

That alone can reduce pressure to act quickly.

3. Add small, temporary income

Even part-time work can extend your runway significantly.

It doesn’t need to replace your full income—just support it.

4. Set up access to equity before you need it

A home equity line of credit (HELOC) is often easier to qualify for while you’re still employed.

You don’t have to use it—but having it gives you options.

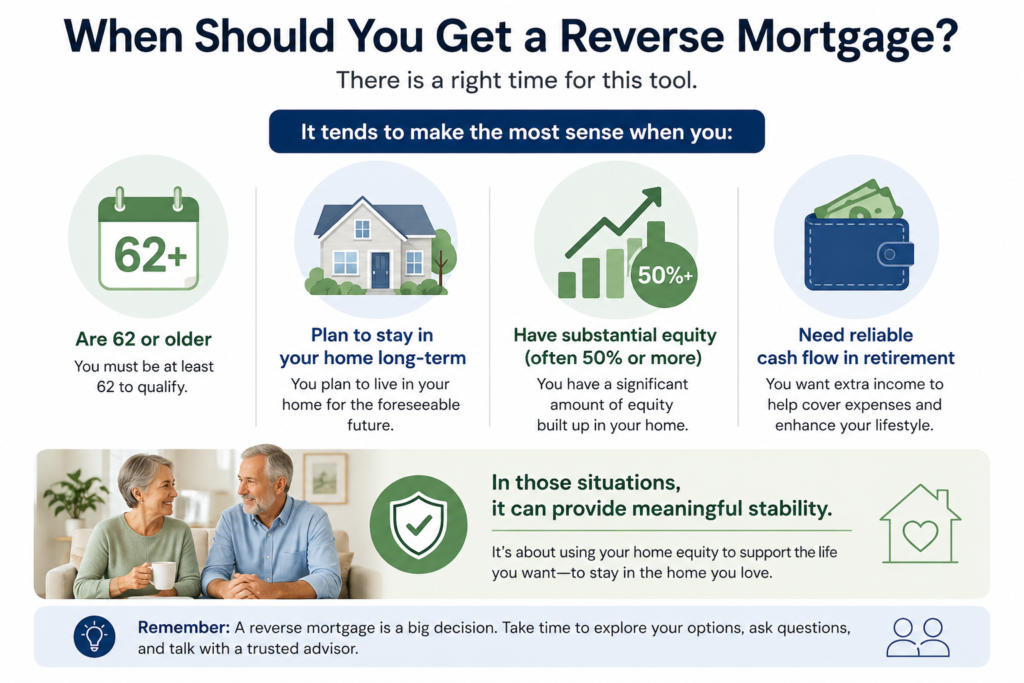

When Should You Get a Reverse Mortgage?

There is a right time for this tool.

It tends to make the most sense when you:

- Are 62 or older

- Plan to stay in your home long-term

- Have substantial equity (often 50% or more)

- Need reliable cash flow in retirement

In those situations, it can provide meaningful stability.

⚠️ Watch Out: The “Emergency Decision” Trap

This pattern shows up more often than you’d think.

Something changes.

Income feels uncertain.

And suddenly, a big decision feels urgent.

But most of the time…

…it isn’t.

You’re not out of options—you’re just early in the decision.

Reverse Mortgage FAQs

What is the minimum age for a reverse mortgage?

For most government-backed reverse mortgages (HECMs), you must be at least 62 years old.

Some private options exist for younger borrowers, but they often come with higher costs and stricter terms.

Do you still own your home with a reverse mortgage?

Yes—you still own your home.

But you must:

- Live in it as your primary residence

- Pay taxes and insurance

- Maintain the property

Do you have to make monthly payments on a reverse mortgage?

No monthly mortgage payments are required.

However, you’re still responsible for taxes, insurance, and maintenance.

How much money can you get from a reverse mortgage?

The amount depends on:

- Your age

- Your home’s value

- Current interest rates

In general, the older you are and the more equity you have, the more you may be able to access—but it’s usually only a portion of your home’s value.

How is a reverse mortgage paid back?

The loan is typically repaid when:

- You sell the home

- You move out

- Or the last borrower passes away

In most cases, the home is sold to repay the balance.

Can you lose your home with a reverse mortgage?

Yes.

You can still face foreclosure if you:

- Don’t pay property taxes

- Let insurance lapse

- Fail to maintain the home

Is a reverse mortgage a good idea?

It depends on your situation.

It can work well for long-term retirement stability—but it’s usually not the best first step for short-term income uncertainty.

What are alternatives to a reverse mortgage?

Common alternatives include:

- Using savings strategically

- Adjusting spending

- Part-time income

- HELOCs

- Downsizing

These often preserve more flexibility.

Does a reverse mortgage affect your heirs?

Yes.

Because the loan balance grows over time, there may be less equity left in the home.

Heirs typically sell the home or refinance to repay the loan.

A reverse mortgage isn’t good or bad.

It’s a tool.

But it’s a tool best used:

- Later, not earlier

- Deliberately, not reactively

- As part of a plan—not a response to fear

Your home equity is powerful—but it’s also finite.

You don’t need to solve this today…

…but you do want to understand it before you ever have to.